Introduction: Gujarat, one of India’s industrially progressive states, recently announced revisions to its minimum wage rates, effective from April 1st, 2024, to September 30th, 2024. These revisions play a crucial role in safeguarding the rights and livelihoods of workers across various sectors.

Key Changes and Impact: The revised minimum wage rates aim to address the rising cost of living and ensure fair compensation for workers. The changes encompass different categories of workers, including skilled, semi-skilled, and unskilled laborers, across various industries such as manufacturing, agriculture, construction, and more.

Sector-wise Updates:

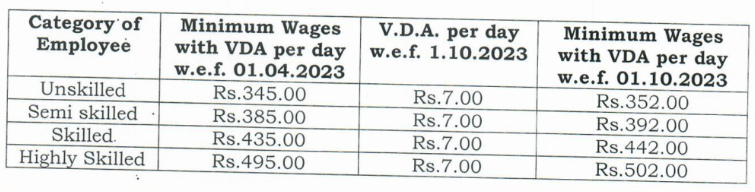

1. Manufacturing Sector:

- The minimum wage rates for workers in the manufacturing sector have been revised to reflect the prevailing economic conditions and inflationary pressures.

- These revisions aim to provide adequate remuneration to workers while maintaining the competitiveness of the industry.

2. Agricultural Sector:

- Farm laborers play a pivotal role in Gujarat’s agriculture-driven economy.

- The revised minimum wages in this sector aim to address the challenges faced by agricultural workers and ensure their economic well-being.

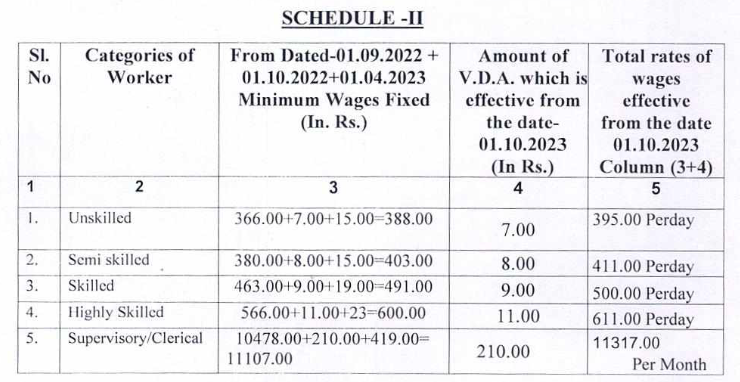

3. Construction Sector:

- The construction industry, a significant contributor to Gujarat’s economic growth, relies heavily on skilled and unskilled labor.

- The minimum wage revisions in this sector aim to strike a balance between fair compensation for workers and the industry’s sustainability.

Government Initiatives and Stakeholder Engagement: The Gujarat government’s commitment to ensuring fair wages is evident through regular revisions and consultations with relevant stakeholders. These initiatives foster a conducive environment for both workers and employers, promoting social justice and economic growth.

Challenges and Future Outlook: Despite efforts to revise minimum wage rates, challenges such as enforcement, compliance, and inflationary pressures persist. Addressing these challenges requires a collaborative approach involving the government, employers, trade unions, and civil society.

Conclusion: The recent revisions to Gujarat’s minimum wage rates for April-September 2024 underscore the government’s commitment to promoting social justice and inclusive growth. By ensuring fair compensation for workers, Gujarat aims to create a conducive environment for sustainable development and economic prosperity.

Gujarat Minimum Wages 1st Apr 2024 to 30th Sept 2024 in English 👈 DOWNLOAD

Gujarat Minimum Wages 1st Apr 2024 to 30th Sept 2024 in Gujarati 👈 DOWNLOAD

Courtesy by: PCS Consultancy

Software Solutions Available on:

TDS | PAYROLL | WEB PAYROLL | WEB HRMS | XBRL | FIXED ASSET |INCOME TAX| SERVICE TAX | DIGITAL SIGNATURE | ATTENDANCE MACHINE & CCTV | DATA BACKUP SOFTWARE | PDF SIGNER

“Our Products & Services”

Sensys Technologies Pvt. Ltd.

HO: 904, 905 & 906, Corporate Annexe, Sonawala Road, Goregaon East, Mumbai- 400 063.

Call: +91 766 990 4748

Email: enquiry@sensysindia.com | Website: http://www.sensystechnologies.com

Branches: Delhi & NCR | Pune | Bangalore | Hyderabad | Ahmedabad | Chennai | Kolkata