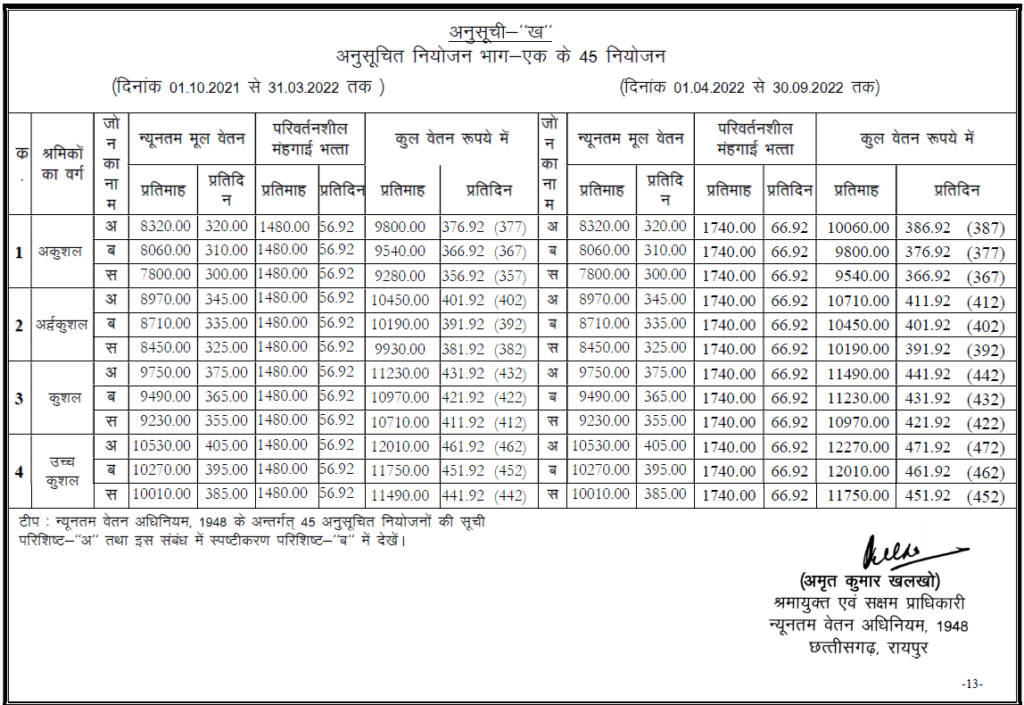

Gujarat Minimum Wages has been revised from 1st April 2022 to 30th September 2022.

GUJARAT CIRCULAR

Gujarat special allowance (1st Apr 22 – 30th Sept 22) ![]()

ENGLISH VERSION

Gujarat Minimum Wages (1st Apr 22 – 30th Sept 22) ![]()

SOURCES BY PCS BLOGS

Gujarat Minimum Wages has been revised from 1st April 2022 to 30th September 2022.

GUJARAT CIRCULAR

Gujarat special allowance (1st Apr 22 – 30th Sept 22) ![]()

ENGLISH VERSION

Gujarat Minimum Wages (1st Apr 22 – 30th Sept 22) ![]()

Following Section 203A of the Income Tax Act, 1961 Form 49B, as per the Income Tax Act of 1961, is a required document to fill out if an individual seeks to obtain their TDS number. People who don’t have a TAN but use TDS deduction are likely to be penalized with a fine of Rs 10,000.

Therefore, the ability to fill out this form promptly is crucial. Another reason this form is crucial is since banks can deny the execution of transactions when the person paying is not an account number.

It is essential to ensure that accurate and complete information is entered on form 49B to avoid rejection.

TAN, also known as a tax deduction and collection account number an alpha number with 10 numbers. It is a number that must be obtained by every person accountable for tax deducting or collecting.

It is required to include TAN in any TDS/TCS return (including any electronic TDS/TCS return) and any payment made through TDS/TCS certificate and TDS/TCS challan. If you plan to be eligible for the TAN, the application to allot TAN has to be submitted in Form 49B.

It will then be presented at one of the Facilitation Centres to receive returns from e-TDS. Addresses of the TIN FC are available at www.incometaxindia.gov.in or http://tin.nsdl.com.

TAN is allocated to the Income Tax Department based on the form submitted at TIN Facilitation Centres operated by NSDL. NSDL will inform the TAN that will have to be included in all future correspondence related to TDS/TCS.

The documents do not have to be submitted in connection with the application to allotment of TAN. But, if the application is submitted online, the acknowledgment generated after completing the application form has to be sent to NSDL. The specific guidelines for this procedure can find on http://tin.nsdl.com.

If a duplicate TAN is allocated, the application can fill for the cancellation of the TAN, which was not utilized by filling out the “Form for Changes or Correction in TAN, which can download from the website of NSDL. (http://tin.nsdl.com) or printed using local printers or downloaded from other sources. The application is also accessible at the TIN Facilitation Centres.

If you have a duplicate TAN is assigned to you, this TAN is to be utilized. The TAN that is used frequently should be utilized. The rest of the TANs should surrender for cancellation using

Form for Changes or Correction in TAN, which can download from the website of NSDL (http://tin.nsdl.com).

TAN is required for every person because without it, Tax Deducted at Source (TDS) or Tax collected at Source (TCS) returns will not be acknowledged by TIN facilitation centres. Banks are not able to accept challans for TDS/TCS payments if the TAN number is not specified.

It is important to note that if you do not submit an application for TAN or do not provide the 10-digit alphanumeric code on specific documents such as TDS/TCS tax returns, eTDS/eTCS returns, TDS/TCS certificates, and TDS/TCS payment challans are subject to a penalty of Rs. 10,000.

Everyone who is required to deduct or collect taxes at the source for the Tax department is required to apply for and get 10 digits of the alphanumeric code TAN.

A Tan card shows the ten-digit alphanumeric number that anyone accountable for a tax deduction or collection must get. The Tax department assigns this number to taxpayers. The tax department allocates this specific number to taxpayers.

Additionally, it is important to know that lenders cannot take TCS or TDS documents if the TAN is not mentioned. Therefore, the absence of a TAN number on official documents could result in Rs10,000 as a penalty.

Thus, those required to deduct tax at the source or collect taxes have to acquire the TAN card. However, those required to deduct tax under sections 194IA, 194-IB, or 194M are not required to apply for TAN.

Before filling out the TAN request form, be aware of its different forms.

The application can be made online on the NSDL-TIN website or downloaded to submit offline. It asks for details like name, address, contact number, nationality, PAN, existing TAN etc. Applicants need to pay a TAN application processing fee of Rs. 65 (Rs. 55 as application charge + 18% GST).

If allotted, the change or correction form requires details like the 10-digit TAN, deductors category, name, address, nationality, and PAN. It also has rows to mention the changes/ corrections required.

Applicants need to prove the allotment of TAN by submitting a TAN allotment letter issued by the IT department or a printout of the TAN details. The fee charged for a correction application is Rs. 63 (plus service tax, as applicable).

You can visit the NSDL-TIN website to apply for TAN. An acknowledgement will appear on the screen at the time of confirmation of the correct uploading of the TAN allotment application.

If an applicant chooses the offline mode, s/he should visit the nearest TIN Facilitation Centre (TIN-FC) and submit the application in Form 49B in duplicate. The addresses of TIN-FC are given on the NSDL-TIN website.

You can submit your online application to the card using these instructions:

Check out the official website.

Form 49B is a long application form consisting of various types of information. Listed below are the form contents that need to be filled out and submitted.

In the end, the applicant has to sign the form or put their thumb impression to verify the form’s contents.

Acknowledgment receipt printout via NSDL website if you’ve completed the form online. If you submit the form in person, there are no additional necessary documents that must submit.

For TAN enrolment, no specific document or identification proof is required. However, obtaining a TAN Form 49B must be completed and submitted. The procedure for registering is explained below:

If you find any data you have entered incorrectly, make it right and submit it online.

No. 341 Survey No. 997/8 Model Colony, Near Deep bungalow Chowk, Pune- 411016

Disclaimer

The information provided in this document is generic and is intended for educational purposes only. This information should not be considered an investment, financial, or tax advice or as an offer or an offer to purchase any investment product.

The Government of Chhattisgarh vides notification NO/08/2022/1897, has revised the VDA effective from 1st April 2022 to 30th September 2022.

THE CHHATISGARH MINIMUM WAGES REVISED NOTIFICATION 1ST APRIL 2022 – DOWNLOAD

SOURCES: PCS BLOGS

Pls find below is the updated ESIC Tie Up Hospital list ( Super Specialty) (Gujarat/Punjab/Chandigarh/Goa)

List of Tie up Hospitals Gujarat Updated – DOWNLOAD

District wise Tie Up Hospital details in Punjab and Chandigarh region – DOWNLOAD

Tie up Hospital list for-providing Super Specialty Treatment and Secondary Level Treatment on a cashless basis for IPs of South Goa and North Goa District in Goa Region – DOWNLOAD

SOURCES BY PCS CONSULTANCY SERVICES

As per the notification dated 8th March 2022 Madhya Pradesh The government has amended the following changes in regards to Restaurant & Eating house an exemption of the following conditions under Section 14- Sub Section (1)

1. Every Employee shall be given one holiday in a week.

2. No employee shall be called for work for more than 48 hours a week.

It will be applicable to the whole state of Madhya Pradesh

MADHYA PRADESH SE AMENDMENT – DOWNLOAD

SOURCES BY PRAKASH CONSULTANCY

| 1 | The Registration in GST is PAN-based and State Specific. |

| 2 | One Registration per State/UT. |

| 3 | However, a Business Entity having separate places of business in a State may obtain separate registration for each of its places of Business. |

| 4 | GST Identification Number called “GSTIN” – a 15 digit number and a certificate of Registration incorporating therein this GSTIN is made available to the applicant on the GSTN Common Portal. |

| 5 | Registration under GST is not tax specific, i.e., single registration for all the taxes i.e. CGST, SGST/UGST, IGST, and cusses. |

The Governor of Punjab vides notification dated 3 March 2022 formulates a scheme for the shops and establishments in the state by which exemption from Section 30 (conditions of employment of women) of the Punjab Shops and Commercial Establishment Act 1958 is granted. The exemption will be given on a case-to-case basis on receipt of applications from the establishments on the following terms and conditions:-

1. The Establishment must be registered/ renewed under the Punjab Shops and Commercial.

2. Establishment Act, 1958.

3. The total no. of hours of work of an employee in the establishment shall not exceed nine hours on any one day and 48 hours in a week.

4. The spread over-inclusive of interval for rest in the establishment shall not exceed twelve hours on any one day.

5. The total no. of hours of overtime work shall not exceed fifty in any one quarter and the person employed for overtime shall be paid remuneration at double the rate of normal wages payable to him calculated by the hour.

6. The Management will ensure –

1. Protection of women from Sexual Harassment at the workplace.

2. Adequate Security and proper Transport facility to the women workers including women employees of contractors during the evening/night shifts. Ln case the management is not providing transport facility or security through employees directly recruited by him and proposes to provide through service providers then the Management shall execute the Security and Transport Facility Contract with an appropriately licensed/registered Security Agency.

3. Women employees will board the vehicle in the presence of security guards on duty.

4. Security ln-charge/Management have maintained the Boarding Register or computerized record consisting of the Date, Name of the Model & Manufacturer of the Vehicle, Vehicle Registration No., Name of the Driver, Address of the Driver, Phone/ Contact No. Of the Driver and Time of Pickup of women employees from the residence to the establishment and vice versa.

5. Attendance Register of the security guard is maintained by the security in charge/management.

6. Transport vehicle in-charge /security in-charge/management maintains a movement register.

7. No employee of any establishment shall knowingly employ a woman and no woman shall engage in employment in any establishment during six weeks following the day of her confinement or miscarriage.

8. Vehicle does not have black or tinted glasses and also ensure that there are no curtains in the vehicle and occupants of vehicle are clearly visible from all sides.

9. Emergency call nos. Are prominently displayed inside

the vehicle.

10. Driver will not pick up any women employee first for workplace and will not drop her last at home/ her accommodation.

11. Driver will not leave the dropping point before the women employee enters into her accommodation.

12. There is an annual self defense workshop/training for

women employees.

13. In the night shift, minimum of five women employees

shall be employed.

7. The manager of the establishment will be required to abide by the provisions of Sexual Harassment of Women at Work Place (Prevention, prohibition and Redressal) Act. 2013.

Punjab grants exemption to SE from condition of employment of women – DOWNLOAD

SOURCES BY: PRAKASH CONSULTANCY SERVICE

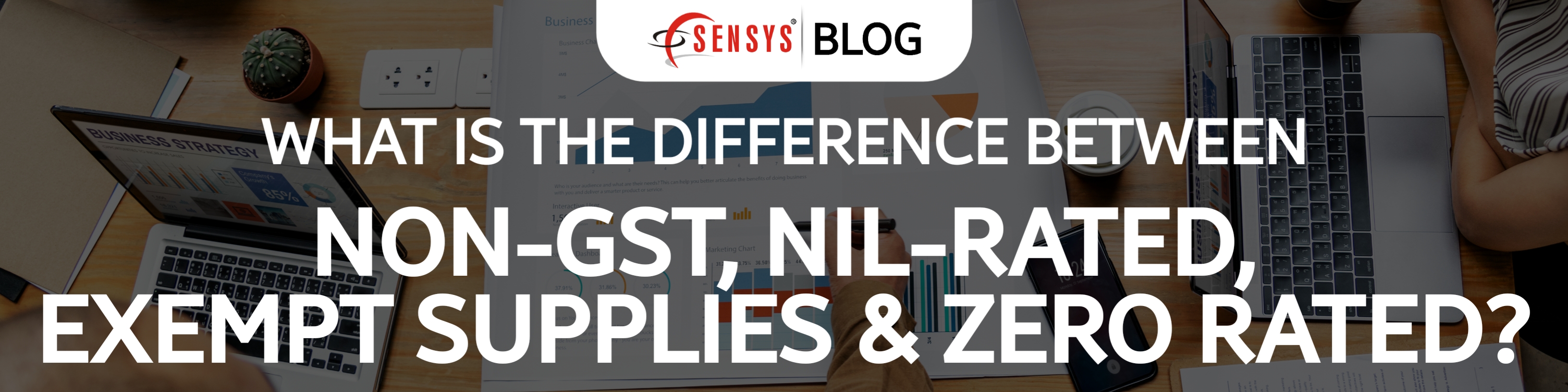

Non-GST Supply

|

| Non-GST Supply means the supply of goods or services or both which is not leviable to tax under GST.

Examples: Electricity, Diesel, Petrol, and Alcohol for human consumption are some examples of non-GST supplies.

|

Nil Rated Supplies

|

| Goods or services on which a GST rate of 0 % is applicable are called NIL-rated goods or services.

Examples: Jaggery, Salt, Grains, Cereals, etc.

|

Exempt Supplies

|

| Exempt Supply means goods and services sold by the companies are free from Goods and Services Tax (GST). Since GST is a tax for the common man, everyday items used by the common man have been included in the list of exempted items.

Examples: Live Fish, Fresh Milk & fruits, unpacked food grains, fresh vegetables, Curd, Bread, etc.

|

Zero Rated Supplies

|

| Zero-rated supplies mean supply of goods or services or both to SEZ or SEZ developer or Export of goods or services or both. GST is not applicable in India for exports. Hence, all export supplies of a taxpayer registered under GST would be classified as zero-rated supplies.

Example: Overseas Supplies and supplies to SEZ

|

MINIMUM WAGES FOR GARMENT 2022-23 – DOWNLOAD

MINIMUM WAGES FOR SECURITY AGENCY 2022-23 – DOWNLOAD

MINIMUM WAGES FOR HOTEL AND RESTAURANTS 2022-23 – DOWNLOAD

MINIMUM WAGES FOR SHOPS AND ESTABLISHMENT 2022-23 – DOWNLOAD

MINIMUM WAGES FOR ENGINEERING-INDUSTRY 2022-23 – DOWNLOAD

SOURCES BY: PCS CONSULTANCY SERVICES

Every supplier of goods and/ or services is required to obtain registration in the State/UT from where he makes the taxable supply if his aggregate turnover exceeds the

threshold limit during an FY. Different threshold limits have been prescribed for various States and Union Territories depending upon the fact whether the supplier is engaged exclusively in the supply of goods, or exclusively in the supply of services or in the supply of both goods and services. The threshold limit prescribed for various States/UTs are as follows:

| States with a threshold limit of 10 lakh for supplier of goods and/or services. | States with a threshold limit of 20 lakh for supplier of goods and/or services. | States with a threshold limit of 20 lakh for a supplier of services / both goods and services and 40 lakh for a supplier of goods (Intra-State). | ||

| ● Manipur

● Mizoram ● Nagaland ● Tripura |

● Arunachal Pradesh

● Meghalaya ● Sikkim ● Uttarakhand ● Puducherry ● Telangana |

● Jammu and Kashmir

● Assam ● Himachal Pradesh ● All other States |